For the last decade, interconnection queues in regions across the country were largely populated by wind, solar, and battery storage proposals due to federal incentives, state renewable energy mandates, flat power demand, and healthy reserve margins that facilitated the growth of intermittent resources while limiting the perceived need for additional dispatchable generation.

However, things have changed substantially, as reliability concerns and surging demand for electricity from data centers have taken center stage in the energy conversation. These new energy realities have reminded policymakers, grid operators, and the power sector writ large that system planning cannot drift far from physical reality without serious implications for reliability and affordability.

Nowhere are these implications more evident than in PJM, where surging capacity prices have spurred a national conversation about how to meet rising capacity needs and mitigate rising costs while integrating more data centers into the regional power system. These new priorities have led to a wholesale change in PJM’s reformed interconnection queue.

Results from the first round of PJM’s reformed interconnection process suggest that rising reliability concerns have reduced demand for new wind and solar projects, as their limited capacity and energy values become more apparent when serving high-load-factor resources is a primary focus. Consequently, natural gas capacity in the PJM queue has surged, with these projects accounting for more projected capacity than wind and solar, combined.

Alongside storage and nuclear, this underscores a simple truth: when reliability matters, markets gravitate toward firm, dispatchable resources—even when federal subsidies and state wind and solar mandates stack the deck against them.

Thanks in large part to the explosive growth of data centers, reliability and affordability are once again the central focus of policymakers.

The New Queue

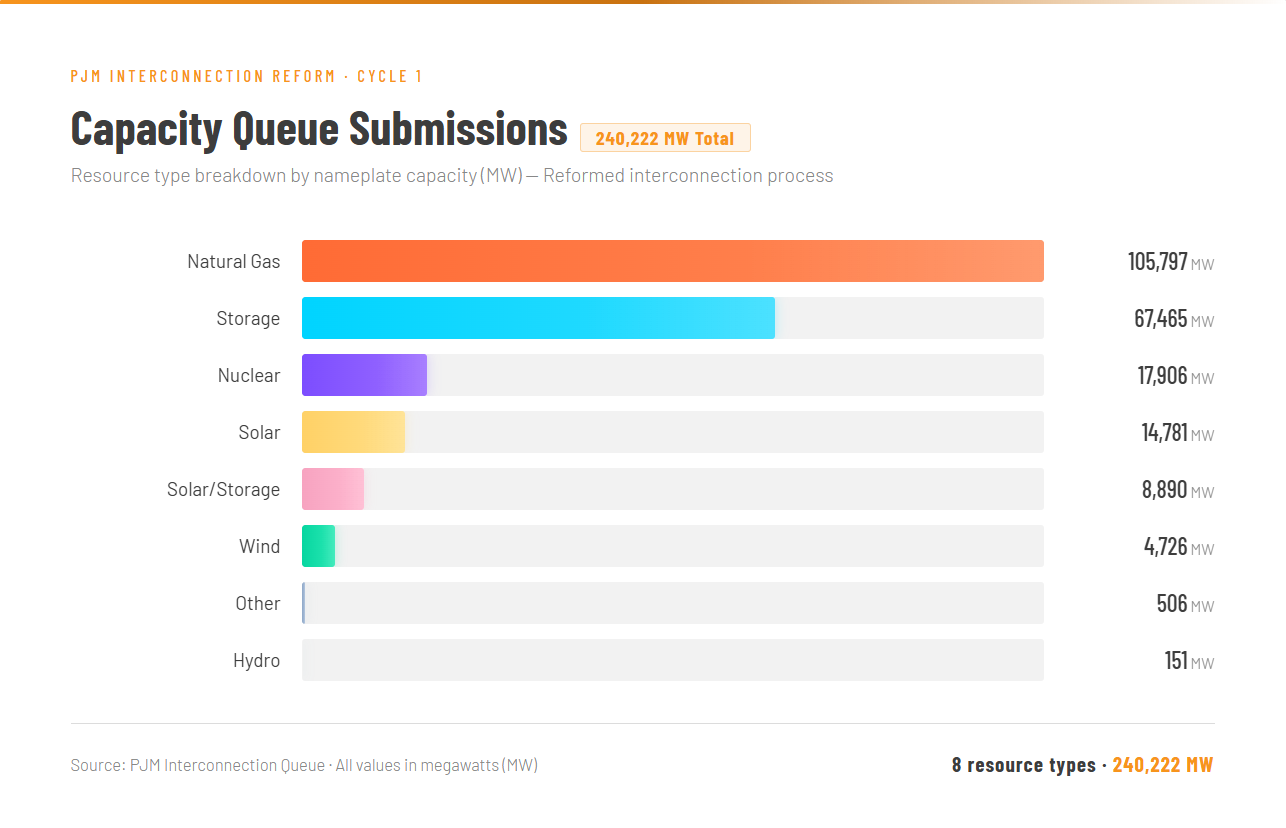

The reformed PJM interconnection queue is prioritizing dispatchability, as natural gas capacity in the queue has reached 105,797 megawatts (MW), with storage and nuclear projects accounting for 67,486 MW and 17,906 MW, respectively. As a result, natural gas queue submissions now outnumber the combined submissions of wind and stand-alone solar by a nearly 4-to-1 margin, shown in the graph below.

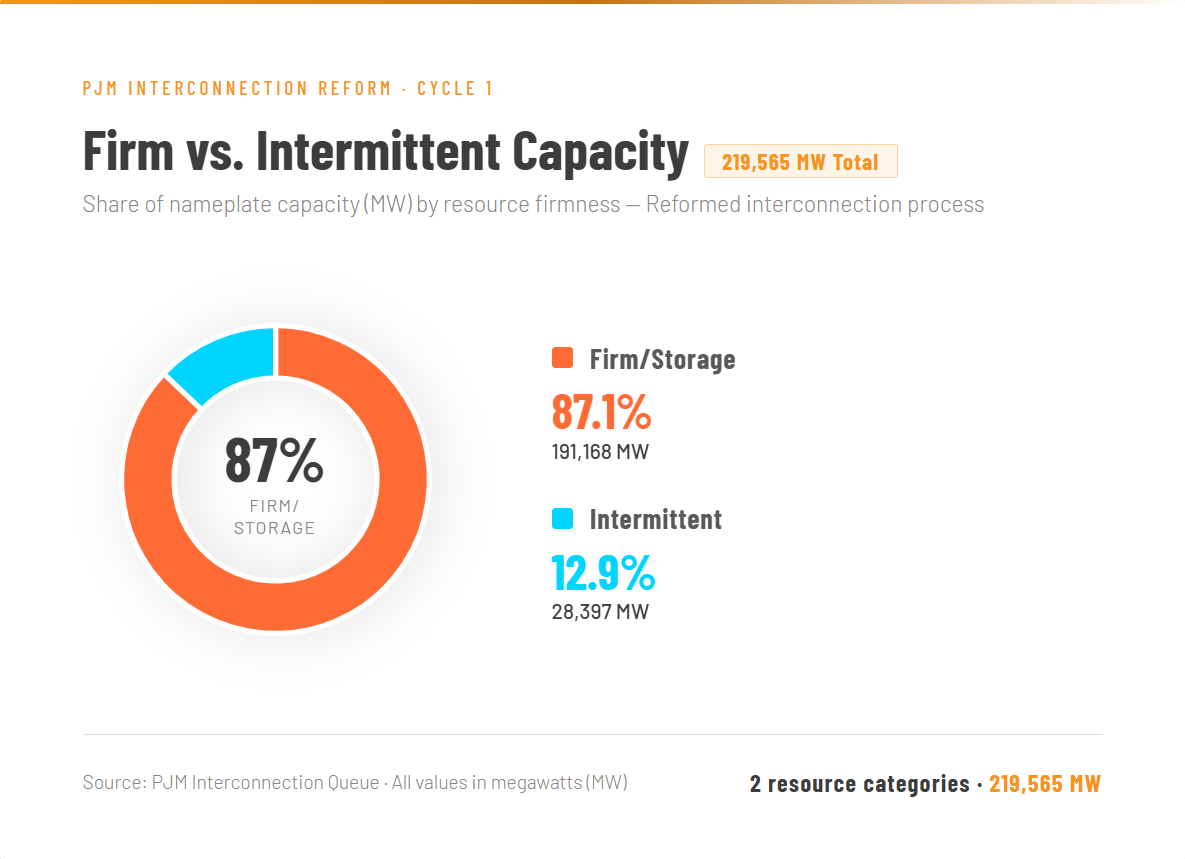

In total, the combined queue capacity of natural gas, storage, and nuclear, all resources meant to deliver firm power to the grid, outnumber wind and stand-alone solar by close to a 7-to-1 margin, shown below.

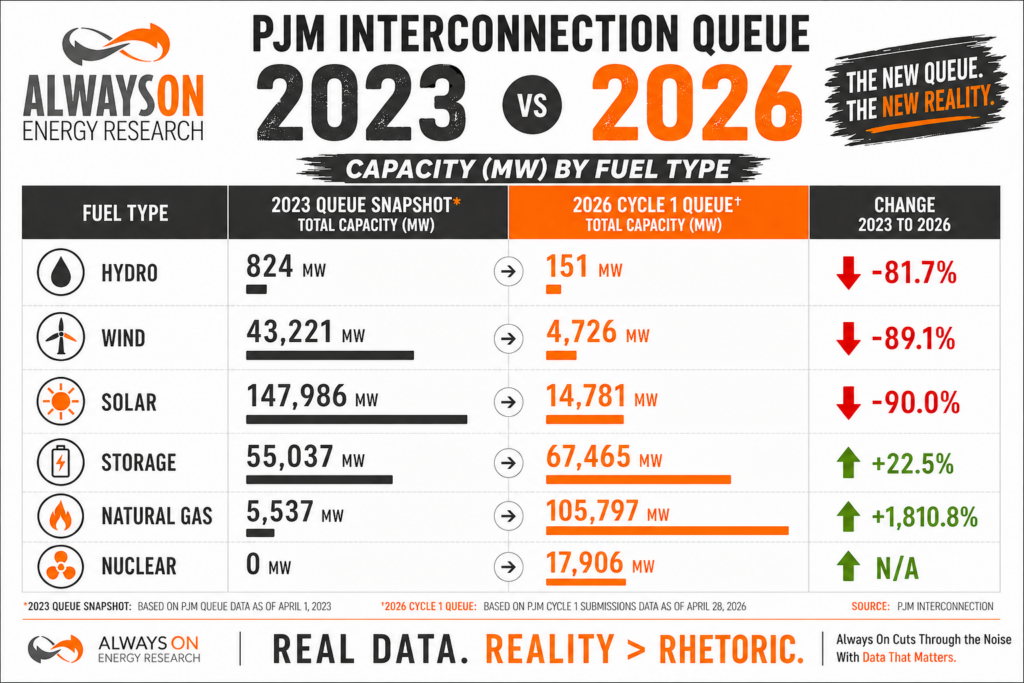

These queue requests represent a dramatic reversal of the PJM interconnection queue as it was constituted in 2023. In that year, wind, solar, and natural gas project submissions were 43,221 MW, 147,986 MW, and 5,537 MW, respectively.

Today, wind projects in the queue are just 4,726 MW, solar is 14,781 MW, and natural gas has surged to 105,797 MW. In percentage terms, wind and solar are down 89 percent and 90 percent, respectively, while natural gas is up 1,810 percent, and nuclear went from 0 to 17,906 MW, as shown in the diagram below.

This demonstrates a growing industry emphasis on electricity availability, leading to increasing orders for natural gas turbines, while leading to fewer future wind and solar projects in the queue.

Surprisingly, even nuclear alone beats standalone solar and wind. While the nuclear total includes a fusion reactor, which we will believe in when we see it, the same idea holds—PJM is in desperate need of reliable generation to meet load growth projections in the near future and to alleviate soaring capacity prices. As a result, it’s turning to all manner of potential resources that can achieve this end.

Soaring Demand and Capacity Prices

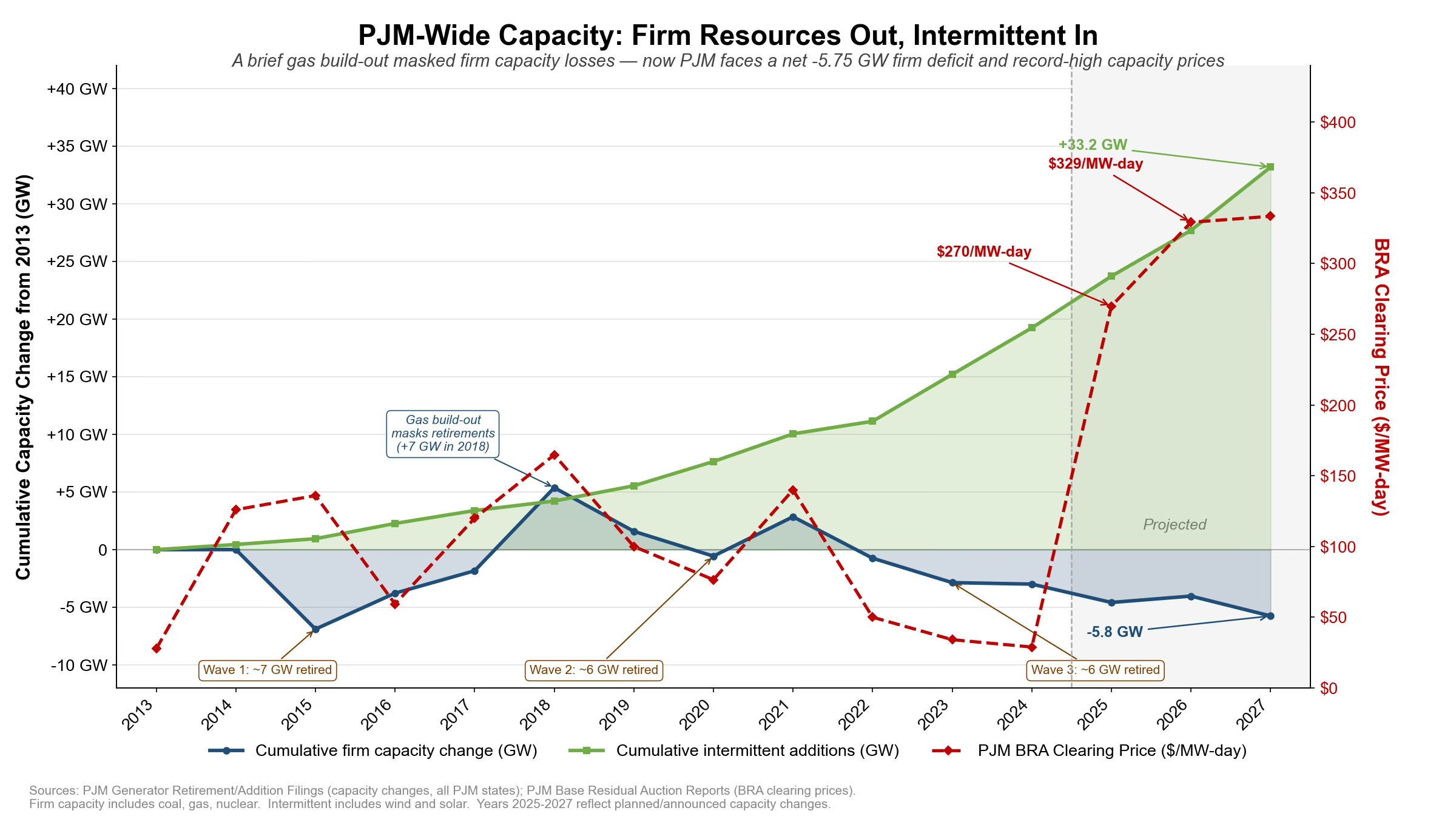

Research from PJM’s Market Monitor, Monitoring Analysis suggests data centers were responsible for an 82.1 percent increase in capacity market revenues for the 2026/2027 RPM Base Residual Auction as demand for power is outstripping supply.

The fact that energy markets are struggling to meet rising demand without burdening residential ratepayers with higher bills is a belated indictment of the energy policies enacted over the previous two decades, rather than a criticism of data centers, as historical data suggest that large-load users helped keep costs low for customers of all rate classes.

Rising demand must be met with additional capacity. However, it is valuable to remind policymakers why regions like PJM are experiencing insufficient capacity in the first place.

Years of flat demand led to complacency. Prevailing energy policies, particularly with respect to coal plants, reduced the once sizable dispatchable reserve margin on the grid. Now, regional grid operators and utilities are struggling to meet load growth expectations that were considered manageable from the 1950s to the early 2000s. Indeed, data centers and other high-load users have placed reliability back where it belongs: at the top of the priority list.

PJM is finding out why it’s so important. Incoming data centers and other large-load industries need power 24/7. At the same time, the system has spent years (and still is) retiring dispatchable capacity and replacing it with resources that make limited contributions during peak conditions.

In a capacity market, when a gap between reliable generators and load growth becomes visible, prices increase. Therefore, rising capacity prices in PJM should not be a surprise, but rather the inescapable economic result of less dispatchable supply, more inflexible demand, and resource additions that do not provide equivalent reliability value.

In this respect, the market is reacting as intended. Despite market distortions that favor intermittent, weather-based resources, these resources have seen sharp reductions in the PJM queue while natural gas capacity has grown. This trend underscores how vital thermal and dispatchable capacity are—that despite decades of unfavorable policies and regulations, they are still standing and refusing to go away.

The opposite appears to be true for wind and solar, as project developers weigh the implications of a soon-to-be-level playing field amid expiring federal tax incentive sand load growth demanding reliable generation. These challenges present a clear rationale for the 89 and 90 percent drops in wind and solar projects from the queue, respectively.

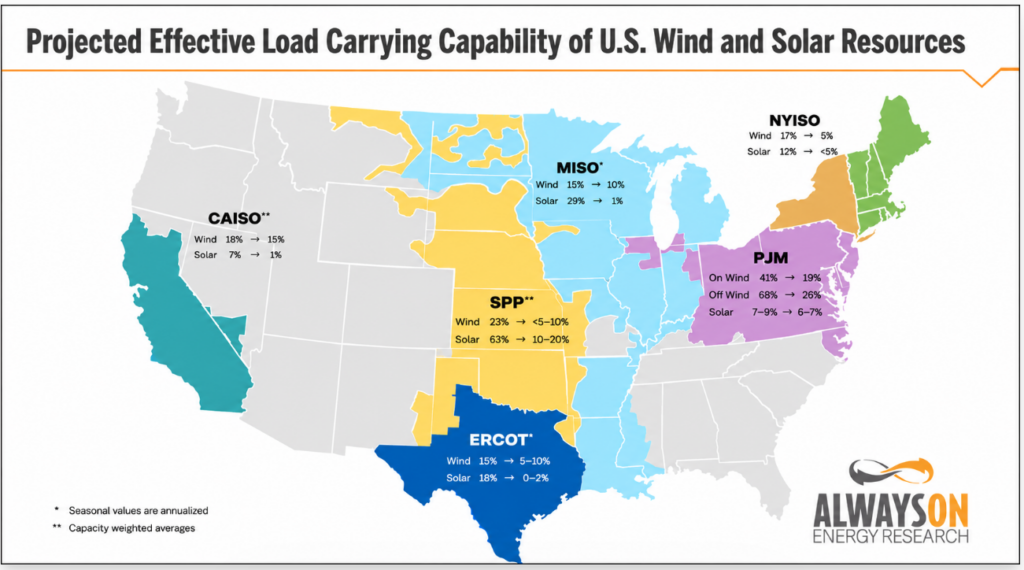

Effective Load Carrying Capacities

Ultimately, capacity markets and integrated utility integrated resource plans are responding to the fact that wind and solar experience declines in their capacity value as more MWs are added to the grid.

Perhaps there is room for wind and solar to be part of the energy mix at very low penetrations (which we are skeptical of), but certainly not for providing the bulk of power production on the grid. The reason is simple physics and mathematics, highlighted by decreasing marginal capacity values.

These diminishing returns were highlighted in our previous piece, More is Less with Wind and Solar.

Wind and solar capacity values fall as more of these resources are added to the grid because their output patterns are often correlated—the sun sets over an entire continent or concentrated wind turbines experience a wind drought—and they are non-dispatchable. As a result, adding more of the same variable resource reaches a point where the resource does not meaningfully contribute to reliability.

…This is reflected by diminishing capacity values for wind and solar in several major regional transmission operators (RTOs) in the country, which we detail below.

This trend is observed in every RTO in the country.

Falling capacity accreditation for wind and solar means these resources are increasingly unable to capture high capacity prices in capacity auctions. This is not a bug; it is a feature of how the capacity markets are designed to work, rewarding resources with high reliability values while less reliable resources receive less revenue.

Conclusion

The previous interconnection process was not prepared to handle surging load growth after years of flat demand and political pressure to prioritize intermittent power plant capacity over coal, natural gas, and nuclear generators.

However, the new energy paradigm of surging demand growth and rising consumer discontent over rising costs has left market participants playing catch-up all at once, rushing to build more reliable natural gas, nuclear, and battery storage, and leaving wind and solar on the sidelines.

This piece was originally published by Isaac Orr and Mitch Rolling on May 2, 2026, at Energy Bad Boys on Substack.