Evergy recently filed its Missouri Metro 2026 resource plan with the Missouri Public Service Commission. It’s 146 pages long, but a few charts demonstrate that Evergy is betting its future on natural gas.

Evergy has a demand problem

The Kansas City-based utility, which serves 1.7 million customers across eastern Kansas and western Missouri, is expecting retail sales to rise 7 to 8% annually through 2030, up from its previous 6% growth forecast.

Evergy is expecting major growth in electricity demand, like many other utilities (if not most of them). Evergy’s contracted large-load electric service agreements total 2.5 GW, up from 1.9 GW in just three months.

However, the Missouri Metro IRP includes only “three specific large load customers” that are far enough along in the planning process to account for. The three projects will require about 900 MW at a steady state, 24/7 demand profile.

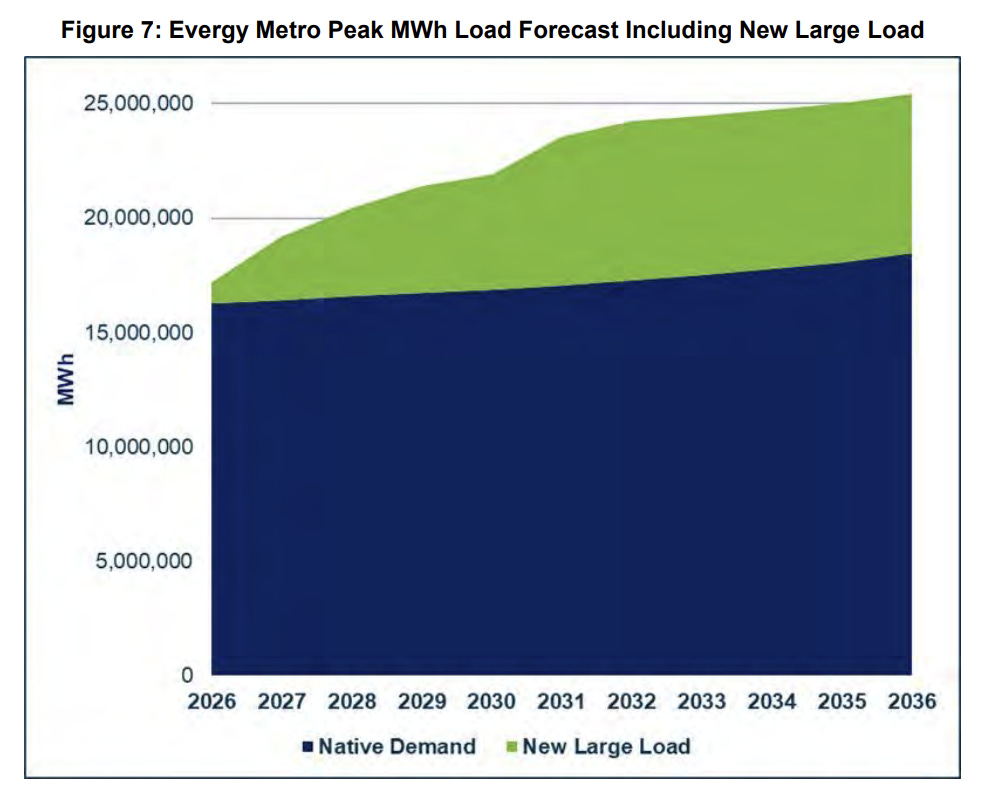

Figure 7 from the IRP shows the Evergy Metro’s Peak MWh load forecast. Total demand grows from about 16 million MWh to over 25 million MWh by 2036 — a more than 50% increase in a decade. The green area is new large-load demand, mostly data centers, growing from a sliver in 2026 to roughly 40% of the system’s total energy requirements.

Every planning scenario in the IRP — low, mid, and high — includes these loads ramping on the same timeline. And the filing flags “strong potential for even greater future load growth,” citing a pipeline of additional customers interested in locating in Evergy’s service territory beyond what is already contracted.

Here’s what Evergy wants to build to meet that demand.

Hello, natural gas

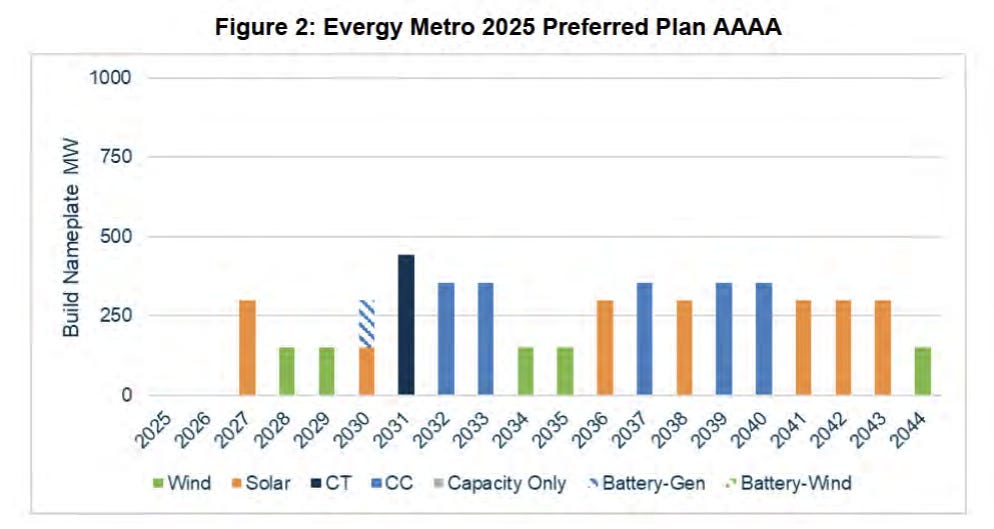

One year ago, Evergy Missouri Metro’s preferred plan called for 300 MW of solar in 2027, 150 MW of wind in both 2028 and 2029, and 150 MW each of solar and battery storage in 2030, with the first new thermal resource not planned until 2031. Further out, the 2025 plan selected 450 MW of wind and 1.5 GW of solar between 2034 and 2044.

Look at all of the green (wind) and gold (solar) in Figure 2, the prior IRP that Evergy submitted. There was still some combustion turbine (CT) natural gas capacity planned in 2031, and some combined cycle natural gas, too, but the near- and long-terms were dominated by renewables.

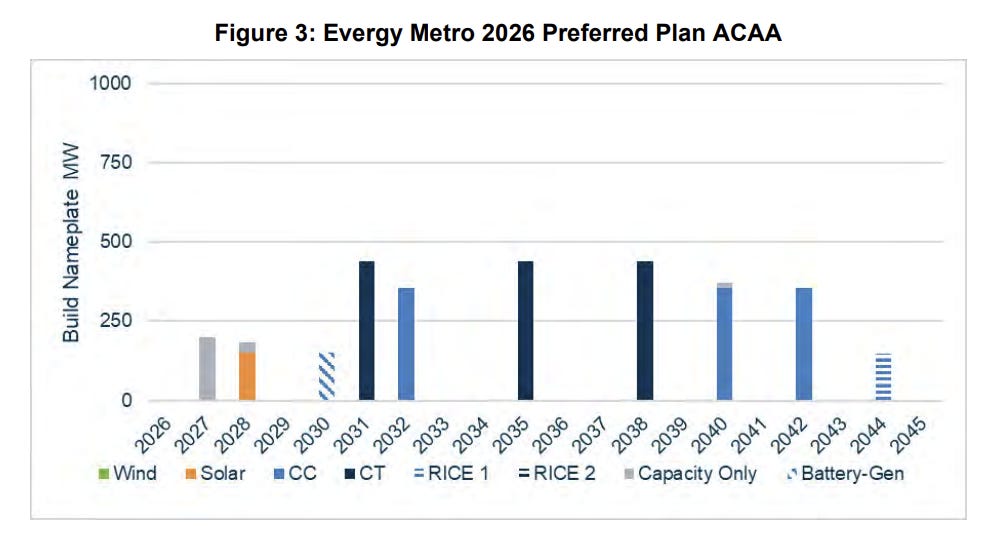

The 2026 Preferred Plan looks quite different.

Wind additions have dropped to zero across the entire 20-year planning horizon. No more green bars on the 2026 chart. Solar plummets to 150 MW in 2028, as this is the only project that qualifies for the production tax credit under current law.

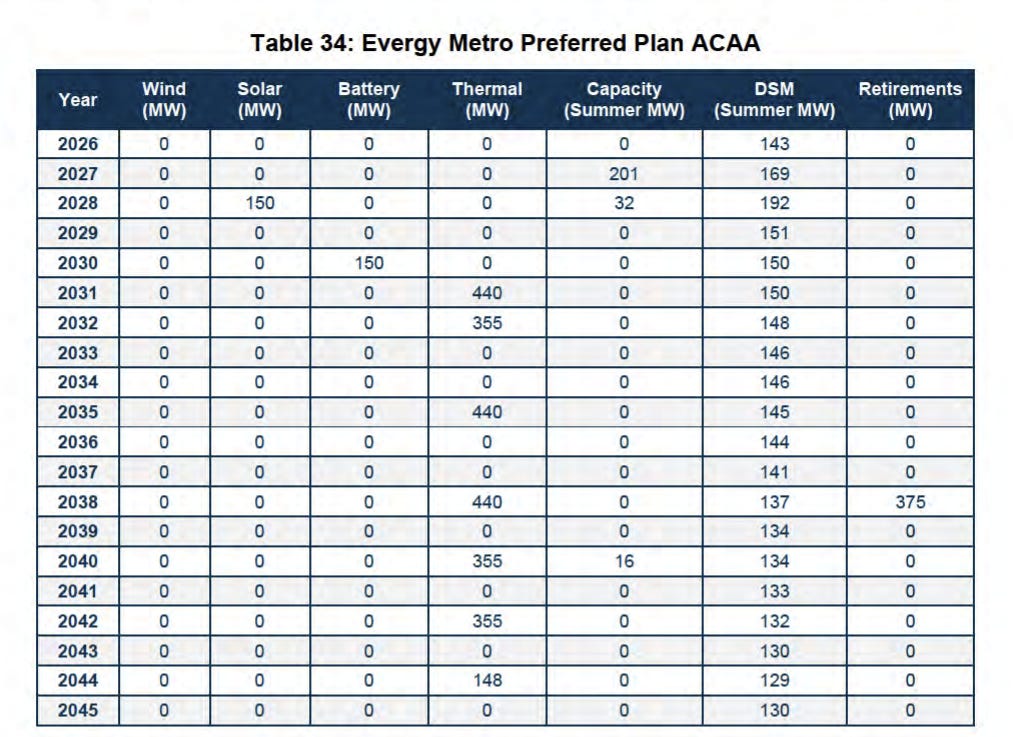

In place of renewables, Evergy selected a simple-cycle gas turbine in 2031, a half-share of a combined-cycle gas turbine in 2032, additional simple-cycle gas turbines in 2035 and 2038, half-CCGTs in 2040 and 2042, and a reciprocating internal combustion engine unit in 2044. Total new thermal generation through 2045: about 2,500 MW.

In fact, Table 34 shows that the only non-thermal additions are 150 MW of solar in 2028 and 150 MW of batteries in 2030.

Evergy notes that their preferred plan is not even the absolute lowest-cost option in their modeling. But the cost difference between this plan and the cheapest alternative is less than $15 million over 20 years, or 0.05% of total revenue requirements. This plan “represents the best risk-adjusted portfolio when factoring the practical realities of project execution,” including “growing permitting challenges for solar development in Missouri.”

Coal retirements are getting pushed back, too

The 2025 plan anticipated retiring the La Cygne 1 coal unit in March 2033 and the La Cygne 2 and Iatan 1 units in March 2040. The 2026 plan delays La Cygne 1’s retirement to March 2038 and pushes La Cygne 2 and Iatan 1 beyond the 20-year planning horizon entirely.

Evergy notes that its coal fleet “continues to be at risk of tightening environmental regulations,” but “the risk balance has shifted due to… rapid load growth, need for reliable dispatchable capacity, higher development costs, and slowing of decarbonization and environmental restrictions.”

These pressures aren’t unique to Evergy. In Colorado, Xcel Energy has asked regulators to allow it to postpone the retirements of all four of its remaining coal units past 2030. Utilities that spent years planning coal retirements around emissions timelines are now discovering they can’t retire coal-fired generation during the fastest demand growth the U.S. power sector has seen in decades.

Wind and solar are no longer competitive

This is what happens when wind and solar have to compete on their own merits.

Evergy identifies the loss of the production tax credit under the One Big Beautiful Bill Act (OBBBA) as a direct “driver of the reduction in renewable resource selections.” Wind and solar facilities that don’t begin construction by July 4, 2026, lose PTC eligibility entirely, and Evergy doesn’t expect wind and solar resources planned for operation in 2029 or beyond to meet the deadline.

Without the subsidies, the economics aren’t there, and that should say something about how “cheap” wind and solar really were to begin with.

The cost trajectory for new construction also isn’t favorable to wind and solar. Evergy’s 2025 all-source RFP, with real bids from real developers, came back approximately 30% higher than previous assumptions.

Even Lazard’s Levelized Cost of Energy+ (LCOE+) report acknowledges that the average unsubsidized levelized cost of onshore wind has risen 49% since 2020, and utility-scale solar is up 54% over the same period. Onshore wind hit its lowest cost, of $50/MWh, in 2021 and has risen to $86/MWh, while solar has bounced up from $41/MWh in 2021 to $78/MWh in 2025.

That’s not to say that gas turbines aren’t also costing more! Evergy forecasts natural gas development costs to be 20-25% higher than forecasted previously, with potentially long lead times. But despite cost headwinds on both sides, Evergy is still choosing gas.

On top of rising costs for renewables, SPP’s new Effective Load Carrying Capacity (ELCC) accreditation method, effective summer 2026, reduces the capacity credit that wind and solar receive as more of each resource saturates the system. SPP’s ELCC is probably closer to the real reliability values of wind and solar.

Evergy’s 2025 preferred plan, with its 450 MW of wind and 1.5 GW of solar, was a product of federal subsidies that masked the true cost of wind and solar. The 2026 plan, which now has to optimize for reliability rather than just the tax code, shows what the economics look like without the thumb on the scale.

A broader pattern

Every utility in the country faces the same OBBBA construction deadline seven weeks from now. And Evergy isn’t the only utility pivoting from wind and solar, though it might be one of the most dramatic.

When PJM reopened its interconnection queue on April 29 after being closed since 2022, gas led with 106 GW of 220 GW in total applications. Wind submissions are down 89% and solar down 90% from 2023, while gas is up 1,810%. Dominion announced a 3-GW gas plant in Virginia. GE Vernova’s gas turbine backlog has hit 100 GW.

Evergy ran the numbers without subsidies, and it’s cut out most solar, and wind entirely. Utilities across the country will be reaching the same conclusion.