The AI hype machine is running at full steam, and the expectation of massive growth in data center load is causing a storm in the energy industry. As the narrative is currently told, data centers are going to devour gigawatts of power, leading to a massive increase in electricity usage and peak demand—with the costs ultimately landing on the broader public.

This has raised endless questions: How will we power them? Can we power them? Should we power them? Will households bear any of the costs? And if utilities build for the boom and the boom doesn’t fully show up, who pays?

These are valid concerns, and we’ve often highlighted how poor decisions of the past have exacerbated the issues. For this article, we wanted to look forward and ask: how likely is the expected data center load to actually materialize, and what assumptions are reasonable when modeling it?

We already know that utilities have several incentives to overestimate load growth projections, and have historically committed forecasting errors that justified massive buildouts of generation resources—only to leave behind stranded assets and ratepayers footing the bill.

Data center demand may be another one of those episodes if anticipated load growth doesn’t materialize.

The Projections: Real or Not?

Forecasting load growth from data centers can be a tricky endeavor. As we incorporate these projects into modeling assumptions, two questions stick out:

- How many of the anticipated data centers will actually be built?

- When built, what will the load factor (or usage) be?

The answers to these questions are major factors for how much capacity utilities will build, how much ratepayers may be asked to cover, capacity factors of generating resources, and how the economics of the broader system shake out.

A recent E3 paper—Forecasting Large Loads in the Age of AI and Data Centers, put it well:

Overestimating growth can lead to overbuilding and stranded costs; while underestimating it can cause reliability shortfalls and congestion. A disciplined approach built on verified baselines, diverse scenarios, adaptive mechanisms, and continuous performance feedback is essential, especially as large and long-term planning and investment decisions are being made based on these forecasts.

That’s the challenge at hand, but let’s first look at what utilities are projecting.

Utility Expectations

The growth of data centers has driven a sharp increase in utility demand forecasts.

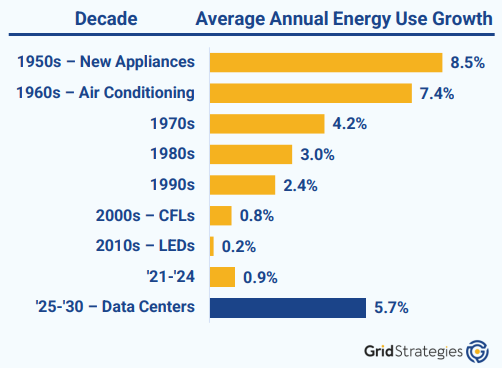

As noted in a report by Grid Strategies:

For the past three years, load growth forecasts have grown at an exponential rate. In 2022 and 2023, manufacturing and electrification shared the stage with data centers. But load growth forecasts for 2025 are now dominated – at least in the near term – by data centers.

The report adds that, if the current forecasts are accurate, “electricity usage will increase at an annual rate of 5.7% per year over the next five years, with peak demand increasing by 3.7% annually during that same period.” That would outpace historical annual growth going back to the 1970s.

We see the same trend in our own work.

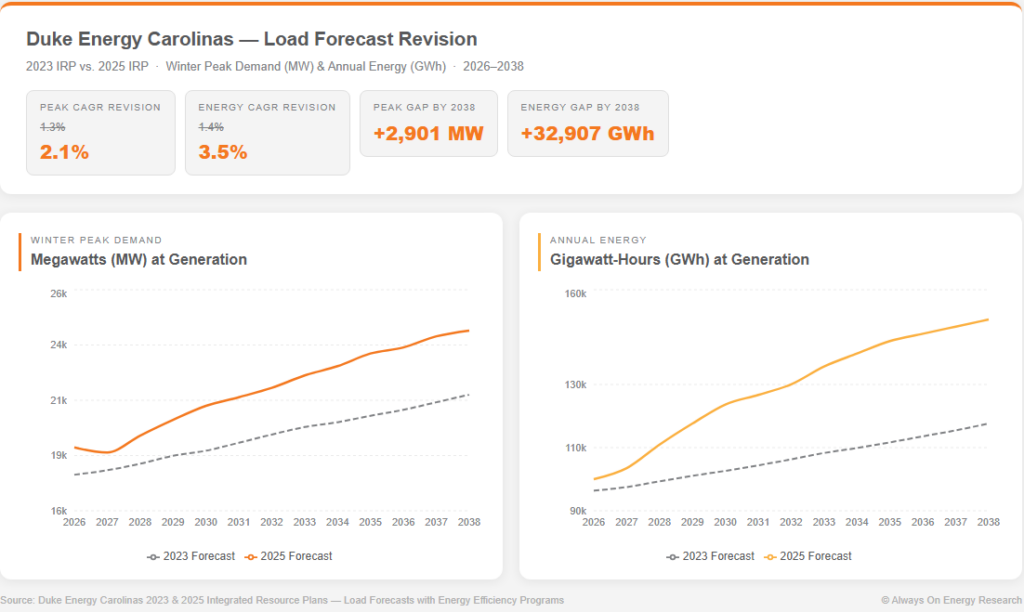

In ongoing analysis of Duke Energy Carolinas, we see that Duke has increased projected load growth by 28 percent by 2038 compared to its 2023 IRP—nearly 33,000 GWh of additional energy—while winter peak demand is up 13.6 percent, or nearly 3,000 MW.

Clearly, growth of that size would require a major buildout of generation and transmission resources—more than has already been occurring. We’ve spent years highlighting how net-zero energy policies drove huge utility investment during one of the slowest load-growth periods in decades. Much of that buildout is poorly matched for rising demand and reliability needs, and now utilities are preparing to spend even more.

The question is whether these forecasts are actually right.

The Uncertainty Behind Data Center Projections

As highlighted by both Grid Strategies and E3, uncertainty surrounds data center load growth expectations, and this matters because assumptions used in planning today become investments tomorrow.

Delayed or Canceled Data Center Projects

The first major uncertainty is: how many proposed data centers will actually get built?

A lot of factors can derail them and slow them down—insufficient power, permitting issues, supply chain bottlenecks, public opposition, or direct legislative action.

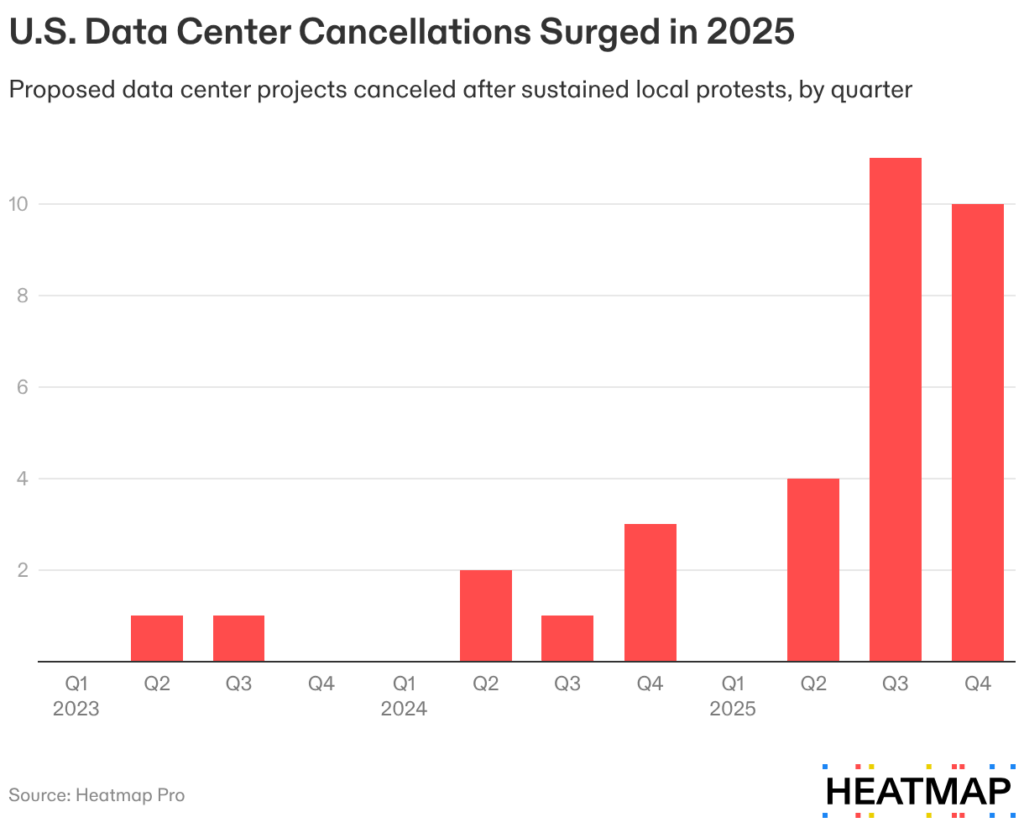

Data Center Watch reported that through March of 2025, “$64 billion of U.S. data center projects have been blocked or delayed by a growing wave of local, bipartisan opposition.” Heatmap reported that cancellations only increased through the rest of 2025.

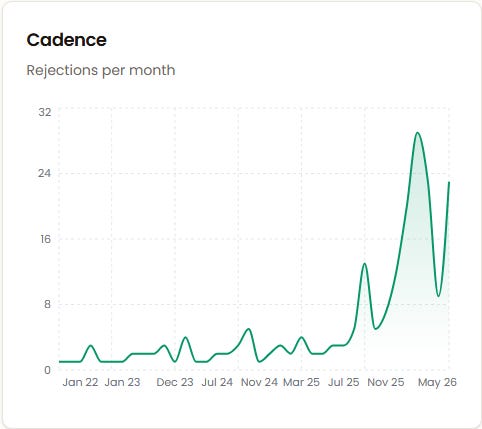

Reporting from our friend Robert Bryce has also documented increasing pushback, including criticism from Pope Leo and a growing list of rejected projects in Bryce’s Data Center Rejection Database. This database shows that rejections per month grew even more going into 2026.

We’ve already witnessed corrections to utility projections.

Georgia Power, for example, cut projected load additions by 6 GW from Q2 to Q3 of 2025 alone. Georgia PSC staff noted that data centers were “primarily underperforming expectations due to a mixture of lower materialization rates, project cancellations, and delays.”

As the testimony further states:

Since the 2023 IRP Update, thirty-three data center projects with 11,332 MW of announced load have been removed from the pipeline, representing ~55% of all project removals, and ~65% of announced load removed.

In another example, AEP Ohio showed how important regulation is to the issue. Interconnection requests fell from 30 GW to 13 GW in 2025 after the PUC in Ohio passed a new data center tariff requiring “data centers to pay for 85% of their requested energy [demand] even if the electricity is not needed at that time.”

While other utilities show trends in the other direction, such as Dominion Energy in Virginia, where demand growth expectations have been consistently growing since 2022—rising from 2.2 percent in 2022 to 6.3 percent in 2025 according to PJM forecasts—the larger point remains:

A request for power is not the same thing as a future megawatt. And when utilities build ahead of load that never shows up, ratepayers are often left paying for the mismatch.

The sudden disappearance of requested interconnections presents a huge challenge for utilities and modeling—as in knowing how much new capacity to build for expected load growth that is elusive—and risk for existing ratepayers, who will be forced to cover the expense if realized load growth is less than what utilities built for.

Load Factors

The second uncertainty is usage. As in, even when a data center gets built, how much will it actually draw?

Most planning assumptions assume load factors (or usage rates) of 80 to 90 percent—well above the broader U.S. grid, which averages closer to 55-60 percent. Grid Strategies notes that “Duke Energy states that it plans for new large loads to have an 80% load factor.” If true, the system will need to prepare for a larger system load factor in addition to a higher peak demand.

This assumption may prove true, but it isn’t a given.

While Dominion Energy in Virginia “reported an 82% load factor for large data centers in 2024,” E3 found that less than half of all data centers in the country reach an 80 percent load factor, and only two reached above 90 percent. Additionally, PG&E published an analysis showing data centers operated at an average of 67 percent.

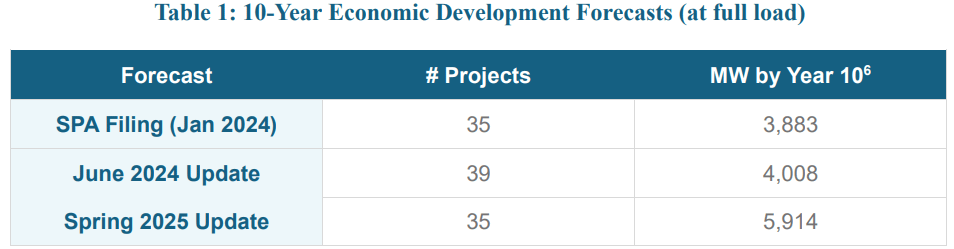

To see how this can completely alter planning assumptions, and therefore investment decisions, let’s examine Duke Energy projections in the Carolinas.

According to planning assumptions for large-load customers updated in the Spring of 2025, Duke is expecting 5,914 megawatts (MW) of new large-load customers by 2034, at full load. This is a 2,000 MW increase from January of the previous year.

Assuming a 90 percent load factor, this would result in 5,323 MW of firm load that Duke would need to prepare the grid for. This value drops to 4,731 MW at 80 percent load factors and 3,962 MW if they operate at 67 percent, highlighting a potential 1,300 MW gap between what could be expected and what may play out.

And this is only one company. Expanded across the country, the MW gap grows to tens of thousands.

The Consequences of Forecasting Errors

The stakes behind accurate forecasting aren’t theoretical.

The best real-world example comes from the 1970s and 80s, when utilities projected nationwide load growth around 7 percent annually, and actual growth landed closer to 3–4 percent. As E3 explains:

As O’Neill and Desai (2003) observed, “assumption drag” prevented models from recognizing signs of slower GDP growth, industrial restructuring, and rising energy prices. When energy costs quadrupled and conservation efforts took hold, electricity demand growth slowed sharply. Utilities, having already committed billions to new capacity, were left with stranded assets and massive overcapacity.

Utilities committed billions toward new generating resources before the reality of diminishing load growth caught up, and this was coupled with inflationary pressures that made plants more expensive to build.

Many plants, mostly coal and nuclear plants, were abandoned in the middle of construction. For the ones that were built, the cost of construction often doubled—sometimes quadrupled—from initial estimates, and many of these opened on grids that didn’t need them anymore. Economic losses totaled in the hundreds of billions.

A 1980 report from the National Regulatory Research Institute provided the following interesting table about nuclear cost overruns at the time:

What to do about recovering the losses was left up to regulators:

Caught in this dilemma, most rate-regulators exercised their authority to fix “just and reasonable” rates by requiring that the huge losses associated with a failed nuclear power project be shared to some degree by both consumers and investors.

The result was decades of bill impacts tied to capacity that was barely used or never used at all. If data center projections miss badly, we could be in for a repeat.

Conclusion (And Possible Solution)

The uncertainty around data center load growth has serious implications for how affordable energy will remain and how prepared the grid will be for load growth.

We see it firsthand in our own modeling work.

Regardless of how accurate the projections are or how much sticking power the demand for data centers will have, the fact is that some of this demand is real—and utilities, businesses, and policymakers are all scrambling to find ways to power them or slow them down.

Meanwhile, the public continues to voice concerns over how they will be impacted by their presence. In the eyes of many, if data centers bring higher electricity costs, that will be all that they bring—the relationship is seen as a net-negative.

Therefore, we need practical solutions to keep costs at a minimum while also powering the needs of the future in a way that doesn’t overbuild the grid now or later on.

One idea comes from our friend Travis Fischer. In this article, he and Glen Lyons make the case for Consumer-Regulated Electricity (CRE), which he describes as “a reform that would allow privately financed, off-grid electric utilities to serve new customers under voluntary contracts,” resolving “a central tension in today’s electricity policy: how to welcome new industrial investment without socializing its costs.” It’s an idea worth considering seriously.

This piece was originally published by Mitch Rolling and Isaac Orr at Energy Bad Boys on Substack, May 30, 2026.