On March 3rd, JPMorgan Chase released its 16th Annual Eye on the Market Energy Paper. This year’s report, written by Michael Cembalest, is titled “Fighting Words,” and it is a 98-page analysis with hundreds of graphs and charts on the state of the energy industry.

It spans most aspects of the energy industry, but as with all things energy, much of this year’s report centers on the impact of data centers on cost and reliability. Also of note are discussions on the cost of solar and storage, conventional fuels, small modular reactors (SMRs), electricity prices, and battery storage economics.

Here are the nine takeaways we found most interesting from the study, hereafter referred to as the JPMC report.

- The Data Center Price Debate: A PJM Deep Dive

Data center impacts on customer costs continue to dominate the headlines for electricity affordability. The JPCM report notes:

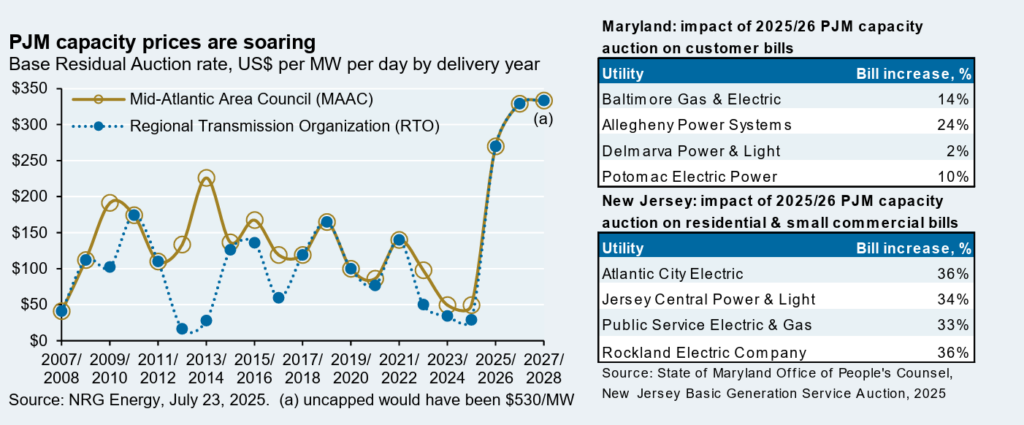

“The PJM region (data center alley: VA, PA, MD, OH) has 67 GW of existing and planned data center capacity, the largest cluster in the U.S. PJM has attracted attention due to spikes in its capacity payments, which are “insurance premiums” paid to generators to commit future supply or commit to demand response reductions during peak demand. Without the cap, the recent PJM auction would have cleared at $530 per MW per day.

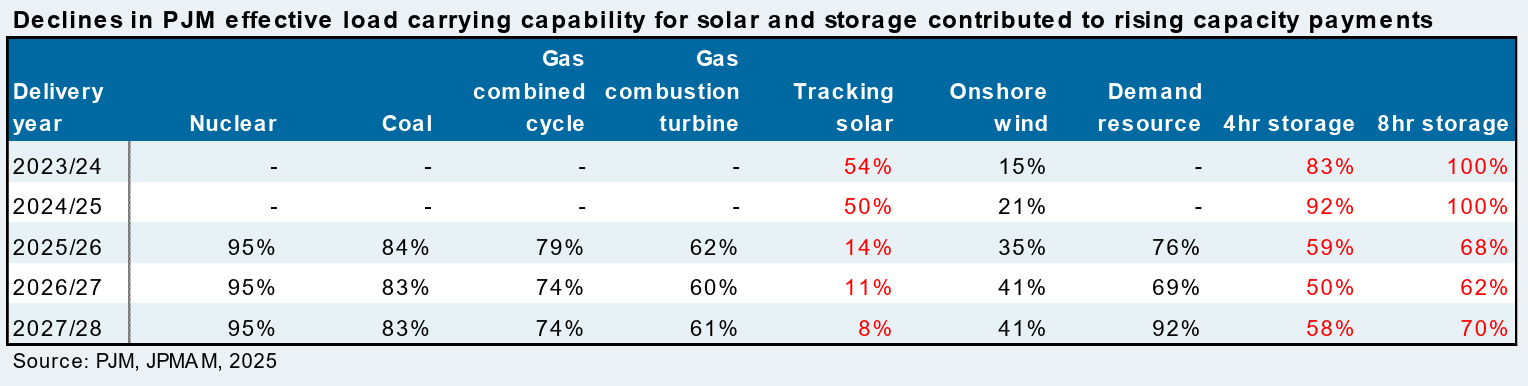

While capacity payments take place in wholesale markets, they’re partially flowing through to retail power prices in MD and NJ. Factors driving the spike in PJM capacity payments include retirement of thermal assets, data centers and declines in capacity accreditation for solar and storage.

Based on the accreditation trends in other regional transmission organizations (RTOs) throughout the country, PJM’s reductions in capacity accreditation for solar and storage were overdue. However, the recent increasein accreditation for onshore and offshore wind seems risky to us because MISO has been its capacity values in the mid-teens.

On a final PJM note, Cembalest seems to think data centers could end the electricity “deregulation” experiment. “Last point: some utilities within PJM are questioning whether re-regulation would be the better option (Exelon, First Energy, PPL, and PSEG); I agree with them.”

2. Data Centers Are Likely Causing Nighttime Load Growth

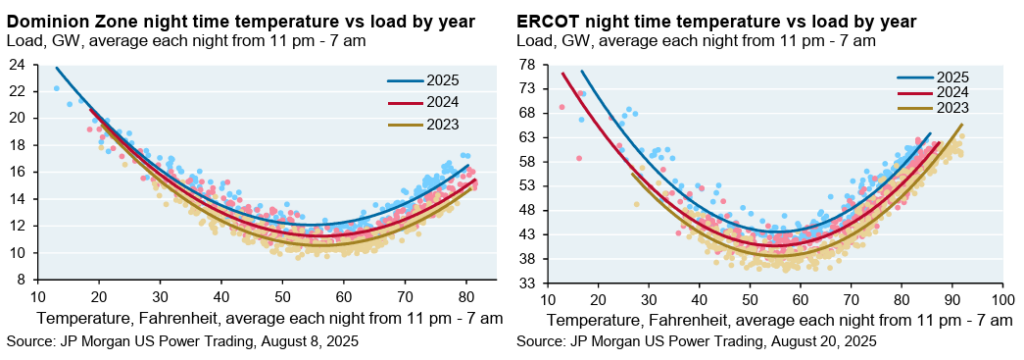

The JPMC report provides evidence that data centers are materially increasing electricity demand at night, which also happens to be the period when the sun doesn’t shine.

Nighttime loads have increased in Virginia and ERCOT since 2023. Nighttime loads are less influenced by industrial production or population. The increase in nighttime loads in data-center-heavy areas such as the Northern Virginia Dominion Zone and ERCOT suggests these facilities are driving evening demand, as JPMC notes, electric vehicles are not drawing enough power to be significant drivers of demand yet.

Cembalest writes “Nighttime load can be viewed as positive as it represents consistent load that allows utilities to monetize capital deployed assets and does not put additional strain during peak hours; but it’s another sign of rising data center demand.”

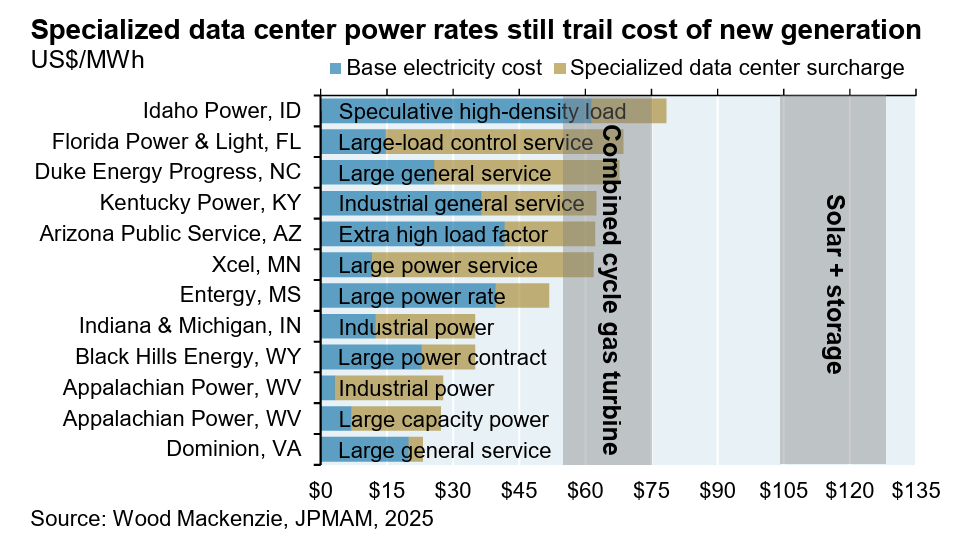

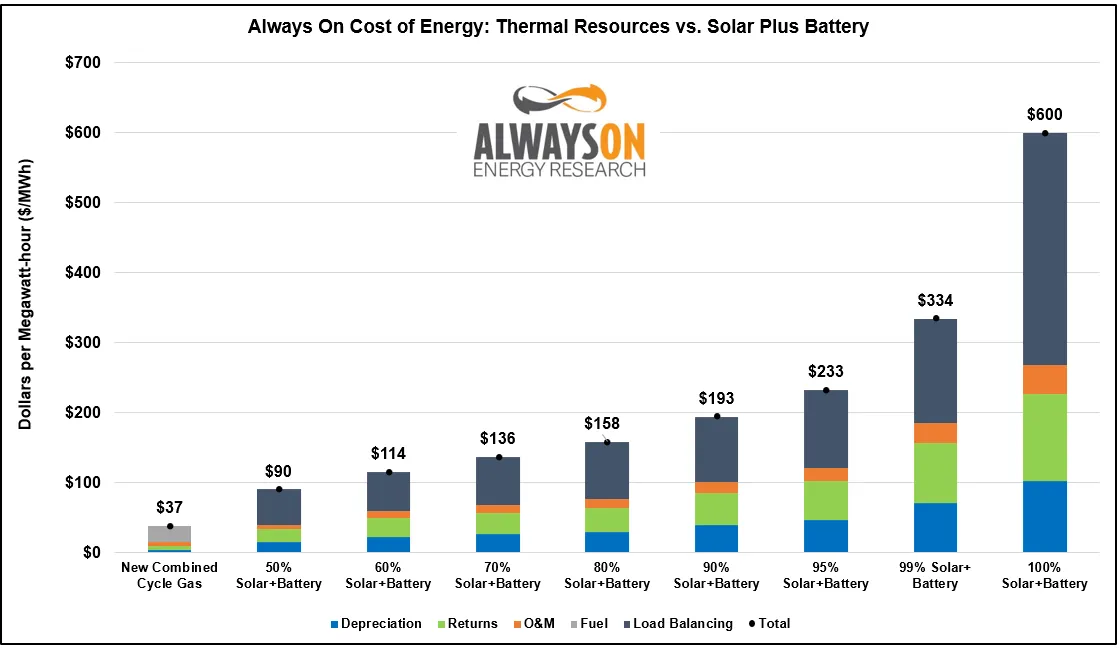

3. Specialized Data Center Power Rates Can’t Afford Solar and Storage

The JPMC report notes seven states have passed or proposed measures to apply higher electricity rates to data centers to account for price impacts on generation, transmission, and distribution costs, and require mandatory participation in curtailment programs under certain conditions.

Despite these efforts, these higher data center electricity rates may not be high enough to completely offset their costs and insulate other ratepayers. Wood Mackenzie published a 2025 report concluding that new specialized rates for data centers may not be high enough to cover the costs of the new generation.

The graph below shows base electricity costs and specialized data center rates from various electric utilities, compared with the cost of new generation for combined-cycle natural gas and solar plus battery storage.

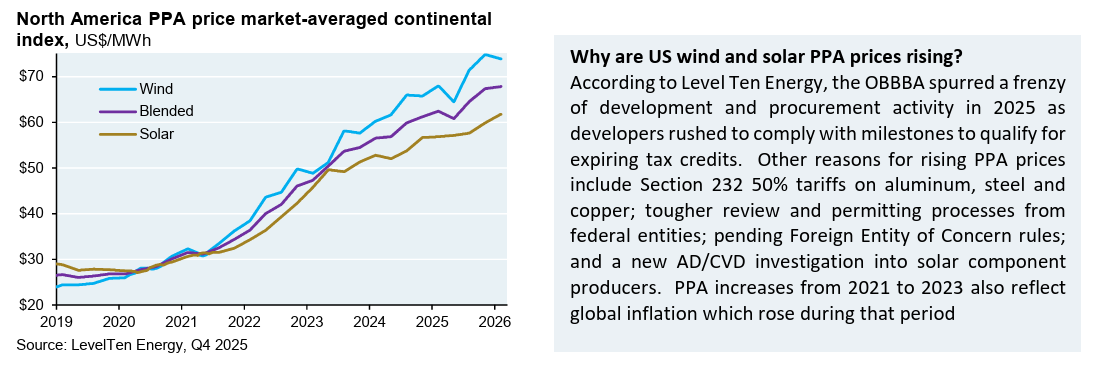

This is particularly true because solar power purchase agreement (PPA) costs keep rising. The JPMC report notes that solar PPA costs, which are subsidized, are over $60 per MWh, a stunning increase from the sub-$30 per MWh deals that were being signed in 2019 and 2020.

It is increasingly looking like the rush to build solar and storage in the United States may go down as one of the largest misallocations of capital in our nation’s history.

Data centers are increasing power demand at night, when solar and storage are unavailable, and they are more expensive than dispatchable, non-energy-duration-limited alternatives.

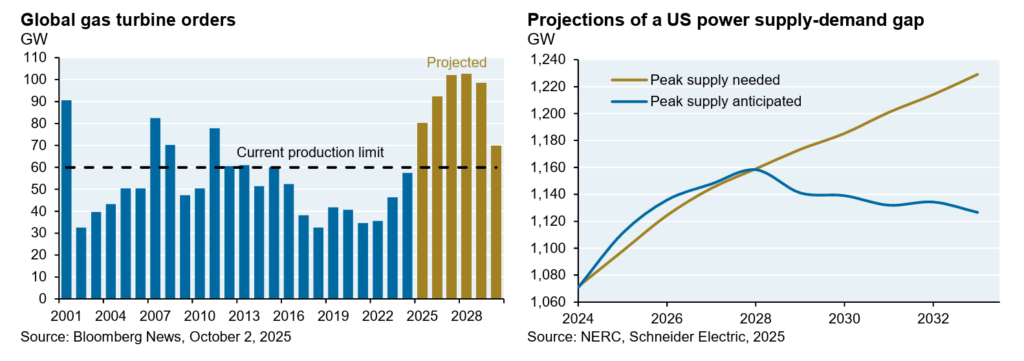

4. The People Want Lots of Gas Turbines

Demand for natural gas turbines now exceeds the current global production capacity through 2030. After years of soft demand for turbines, it appears demand for gas-fired power plants has rebounded in a big way, an unsurprising development given gas costs relative to solar and storage.

Cembalest writes, “Three companies each have 20 to 25 percent of the global turbine market share: GE Vernova, Siemens, and Mitsubishi, and each is planning to expand production. Mitsubishi plans to double production capacity within two years; GE Vernova will ramp annual output from 16 GW in 2023/2024 to 22 GW later this year and to 26 GW by mid-2028; and Siemens Energy is investing $1 billion in US manufacturing, lifting its large turbine production capacity by ~20 percent.”

It remains unclear if this will be enough to clear backlogs as demand is simultaneously increasing.

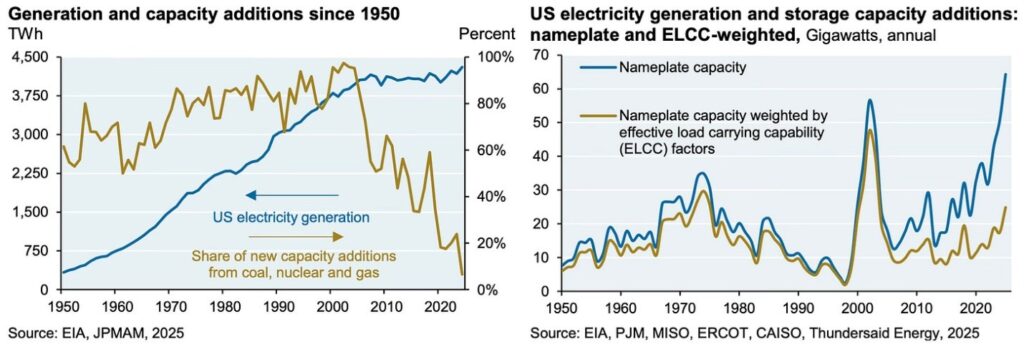

5. Nameplate Capacity is Not Always Reliable Capacity

Electricity demand rose 2-4 percent annually from 1950 through 2006. While grid planners managed to keep pace with this increase, fuel-based resources accounted for the majority of resource additions.

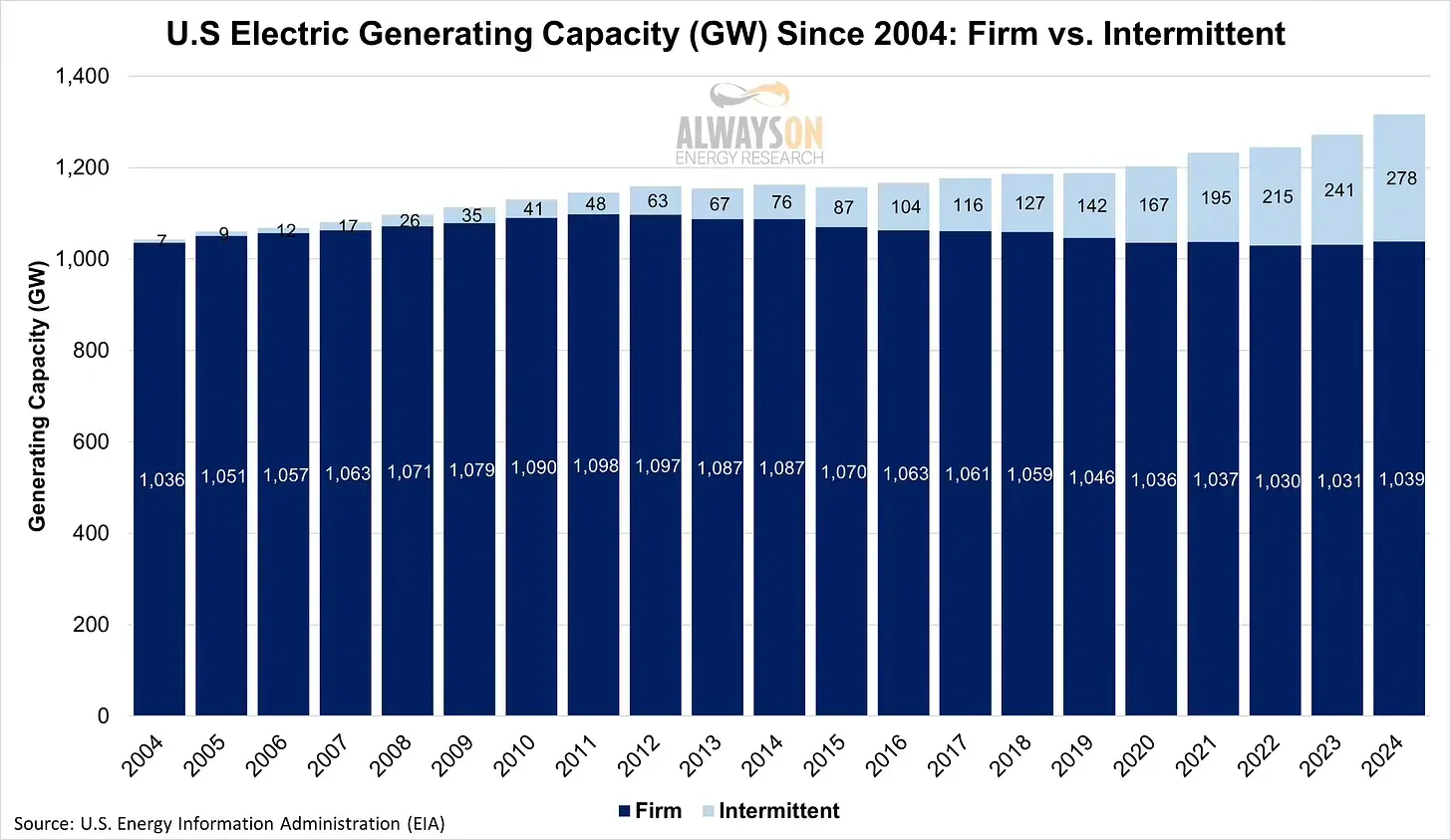

This is no longer the case. Even though the U.S. is building more new capacity annually than ever before, it’s not equating to reliable, firm capacity because new capacity additions are increasingly made up of intermittent wind and solar resources, while coal, natural gas, and nuclear additions have fallen to roughly 10 percent of new additions.

As Cembalest notes:

Whether the same pace can be maintained today is another question, particularly given shortages of skilled energy labor, shortages of transformers, breakers and other equipment and tariffs on grid equipment which do not benefit from the kind of exclusions granted to semiconductors and computers. As shown in the second chart, new US power capacity looks like it’s surging but is a lot more gradual after adjusting for reliability and intermittency (i.e., derating of solar and wind). In other words, not all megawatts are created equal.

AOER analysts described a similar trend in a recent piece entitled Watt, Me Worry? Reserve margins are declining nationally as reliable generators account for a smaller share of new capacity additions, and these additions are not keeping up with thermal retirements.

The result is that “the U.S. is now at pre-2005 levels of firm capacity on the grid at a time when electricity demand is projected to have the largest increases in over a decade due to data center and AI growth and electrification efforts.”

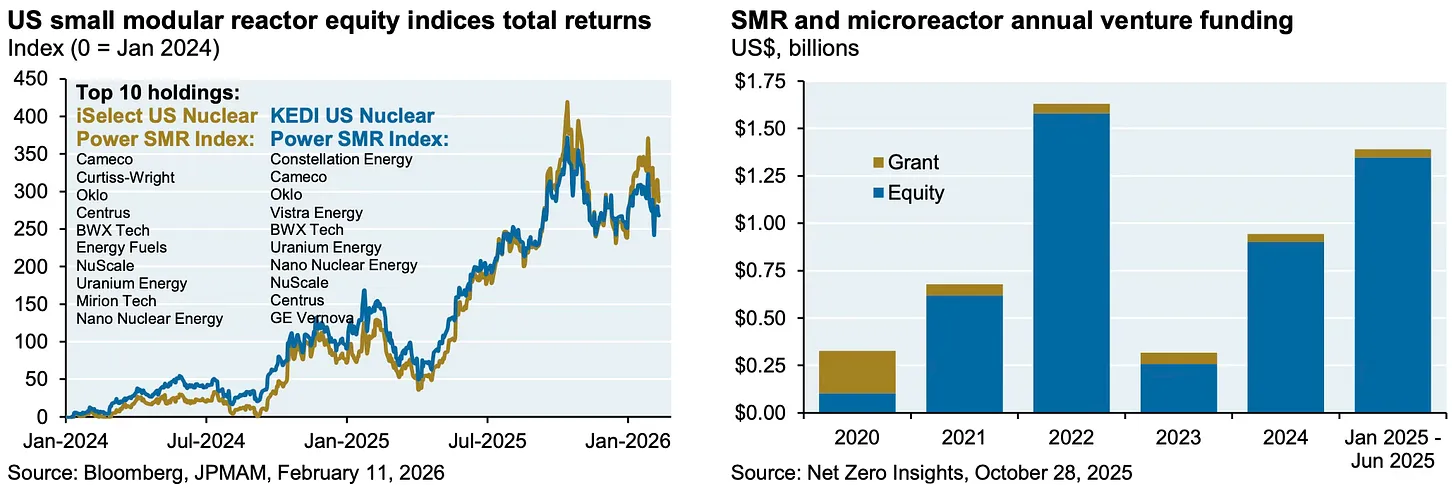

6. The Economics of Small Modular Reactors (SMR)

There is plenty of optimism for SMR technologies to mature into affordable options for the grid, and investors continue to express this optimism with their wallets. SMR stocks have stabilized and annual venture funding remains high.

However, as Cembalest notes, investor optimism doesn’t mean cost-effective, and “burden of proof for economic viability still lay with the SMR industry.”

We stress the fact that any decarbonization campaign is an expensive one, whether using renewable or nuclear technologies. In the case of nuclear, this is because of the incredibly high up-front capital cost to build nuclear power plants.

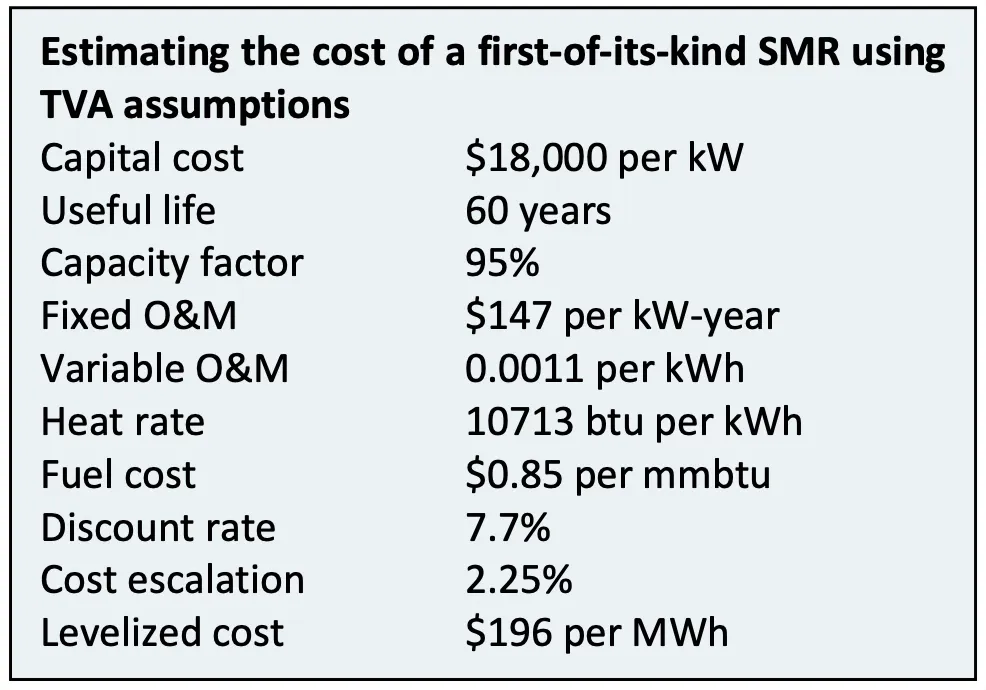

As noted in the report, “A 2025 paper from the former chair of the US Nuclear Regulatory Commission reviewed four SMR types and estimated SMR levelized costs of $200 to $400 per MWh,” and that these surpass that of Light Water Reactors (LWRs) due to diseconomies of scale. Cembalest includes a Tennessee Valley Authority (TVA) analysis of a “first of its kind SMR,” resulting in a price of $196 per MWh—over 50% higher than Cembalest’s upper limit of what he considers “affordable” of $130 per MWh.

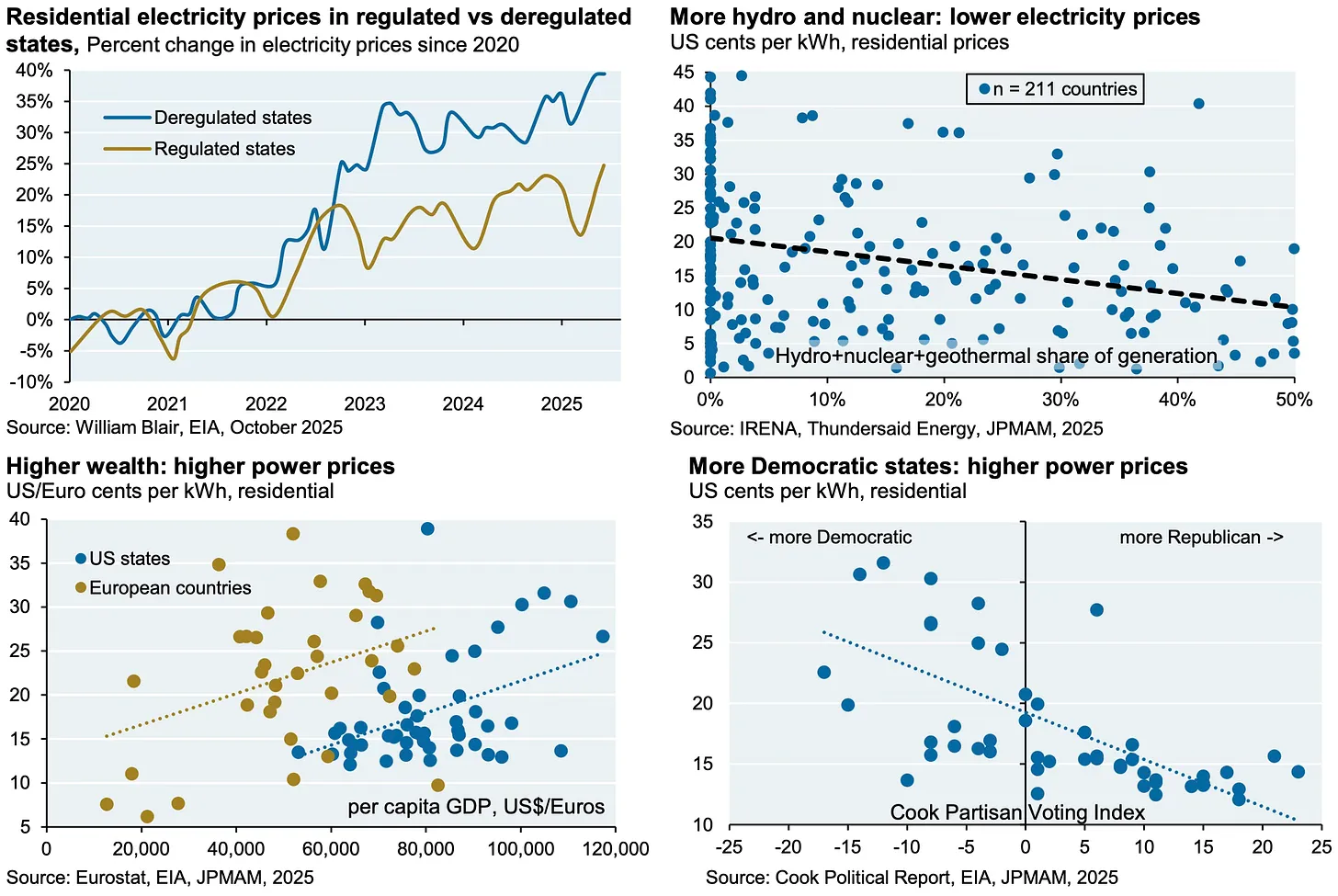

7. Blue States High Rates (And Others)

Cembalest also describes several factors that are correlated with higher electricity prices, including the fact that “Democratic states have higher power prices.” Always On readers will know that we have noted the similar trends.

The remaining four factors include:

- Deregulated states have higher prices than regulated states, which surpassed regulated states in 2022.

- States with more nuclear and hydro have lower prices.

- Wealthier regions have higher prices.

- Regions that rank low in business friendliness have higher prices.

8. Correcting EMBER’s Baseload Solar Analysis

Our readers will remember that Ember, a pro-wind and solar think tank, published an analysis last year claiming that “baseload” solar was now competitive globally with other forms of generation.

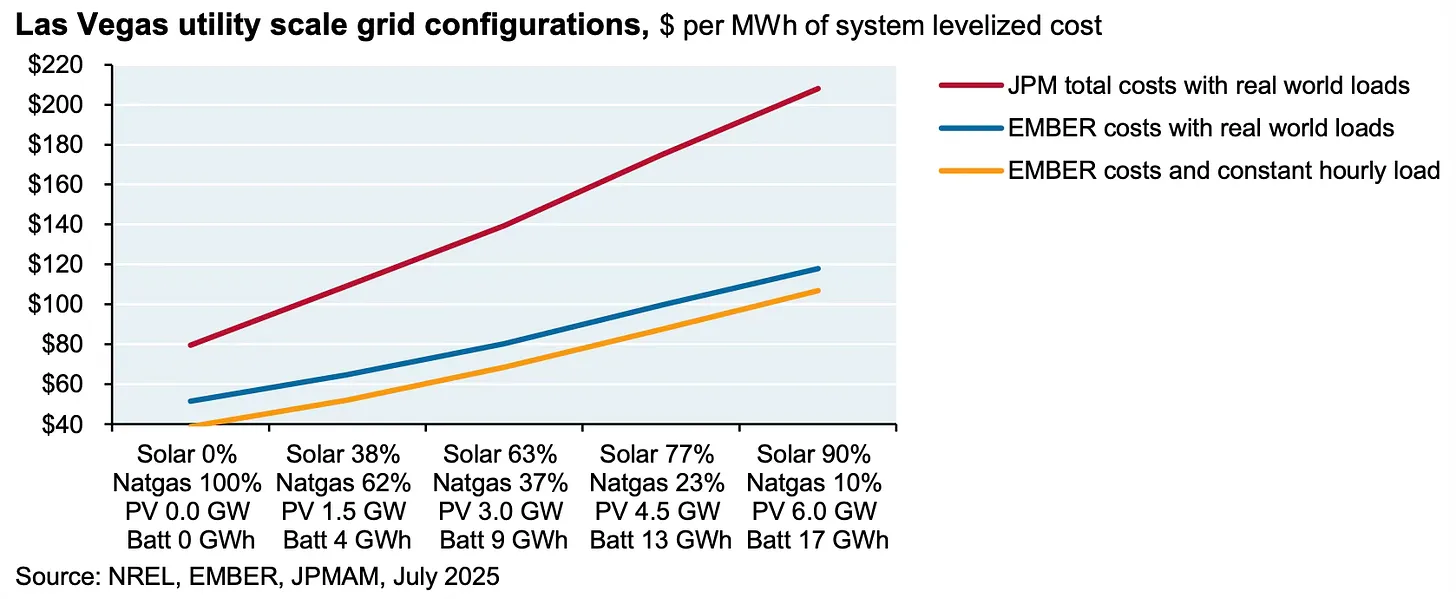

Cembalest is very direct in his criticism of EMBER’s report, concluding that “our analysis mostly rejects EMBER’s thesis and finds that their report understates the economic tradeoffs of deeply decarbonized solar + storage systems in cities like Las Vegas.”

Cembalest notes: “On this kind of topic, stick to peer-reviewed pieces in publications like Joule. EMBER’s article is more a reflection of the world the authors want to exist rather than the world as it really is.”

We actually spoke with Cembalest and his team about Ember’s analysis after we published our article, The “Baseload” Solar Beatdown and our findings were very much aligned, with JMP estimating the cost of 90 percent solar 10 percent gas around $210 per MWh, compared to our estimate of $193 per MWh.

On a final note, the JPMC report examines what would have to happen for solar and storage costs to actually fall below natural gas. Here’s what they found:

What would it take for the unsubsidized cost curve to be flatter, implying a more even economic tradeoff between an all-gas system and the max penetration solar+storage system? Something like this: gas prices rise to $8 per mmbtu, AND solar capital and operating costs fall by 70%, AND 4-hour storage capital costs fall by 70%. While learning curves have been steep, $335 per kW for solar and $68 per kWh for storage seem a long way off, at least in the US. The impact of US tariffs raises the uncertainty further.

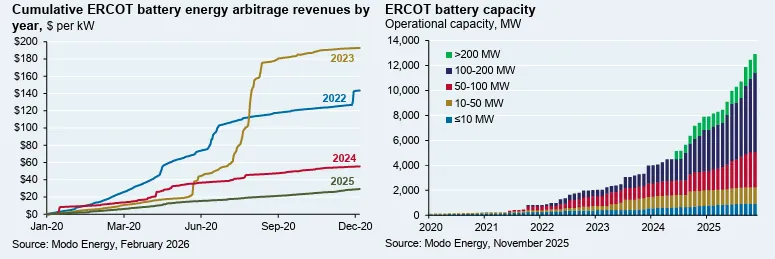

9. ERCOT Battery Arbitrage Revenues Fall

ERCOT’s batteries are starting to resemble the Donner Party—with more capacity flooding the market and cannibalizing the buy-low/sell-high spreads that made storage profitable in the first place.

As the JPMC report notes: “2025 was a bad year for battery revenues. The reason: 9 GW of new battery capacity in ERCOT saturated Ancillary Services and pushed storage into diurnal energy market competition, compressing spreads across the grid and increasing storage capacity by 70x since 2020.”

Falling arbitrage revenue could eventually reduce the incentive for new entrants to the market, and leave the ERCOT region short of juice when it is needed most.

As we have noted previously, ERCOT is in a precarious reliability situation because the system has added no dispatchable resources, on net, since 2004, largely because subsidized wind and solar have driven down wholesale power prices to the point where natural gas investments don’t pencil out.

Battery storage capacity in ERCOT has skyrocketed, from virtually no storage in 2021 to over 12,000 megawatts in 2025. But there is a problem: solar and storage do a pretty good job of meeting summer peak demand, but short-duration storage is entirely unequipped to handle winter storms.

Texas continues to gamble with its grid.

Conclusion

The report contains a multitude of information, but there is no doubt that data centers have entirely reshaped the contours of the energy debate in just 18 months. Policymakers appear to have reprioritized affordability and reliability as public dissatisfaction with rising costs has grown.